Banks Fight For Your Business

As brokers, we shop your scenario with 30+ lenders to get you the best rate.

No Lender Fees

We don't charge any lender fees, saving you on average $1,600 over retail banks.

Won't Impact Credit Score

We make sure the numbers work before running your credit.

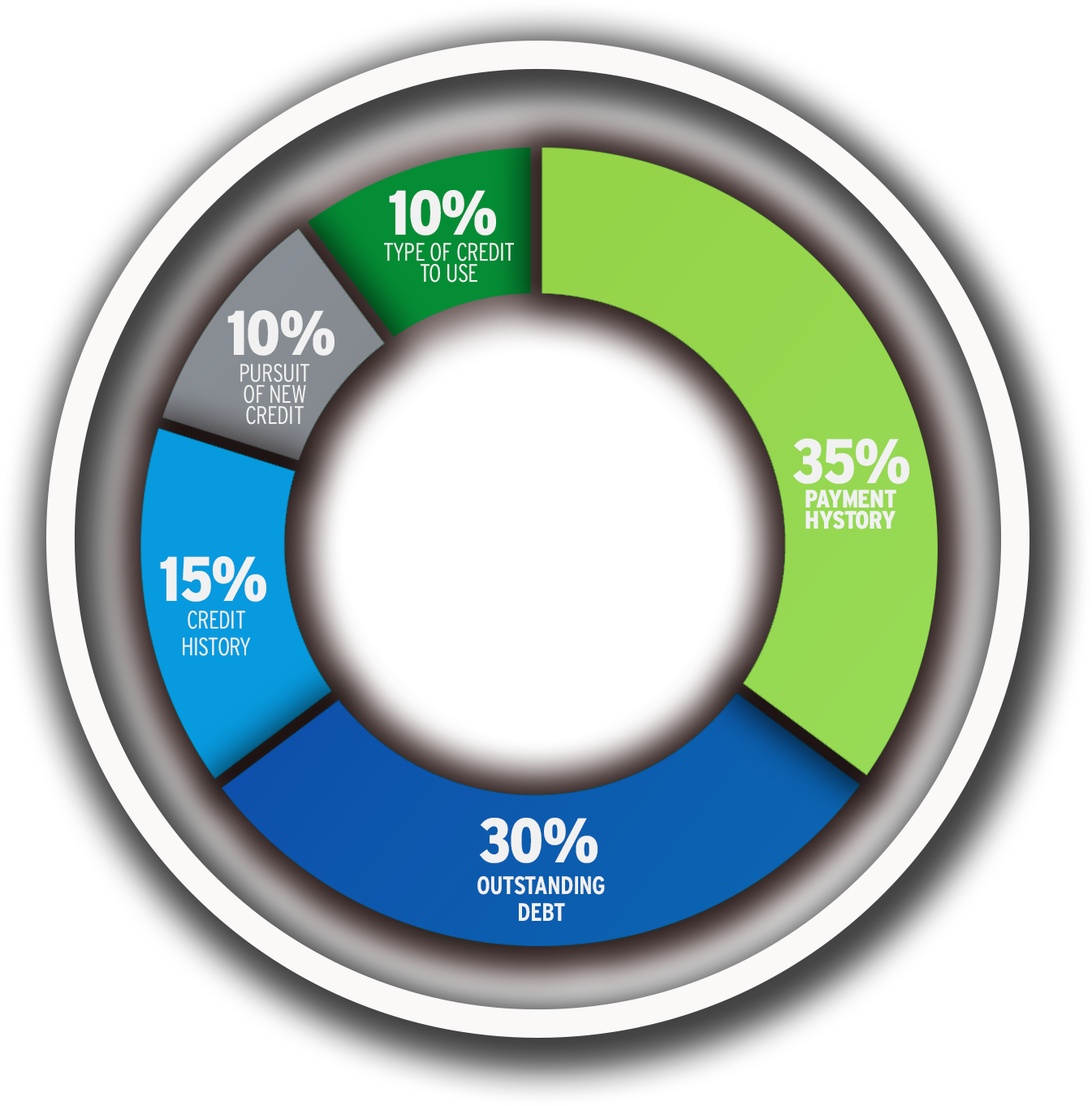

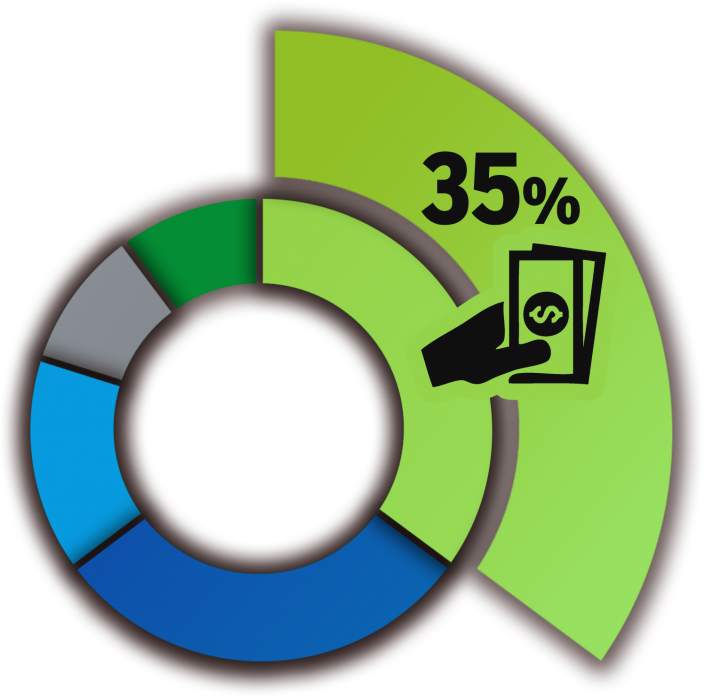

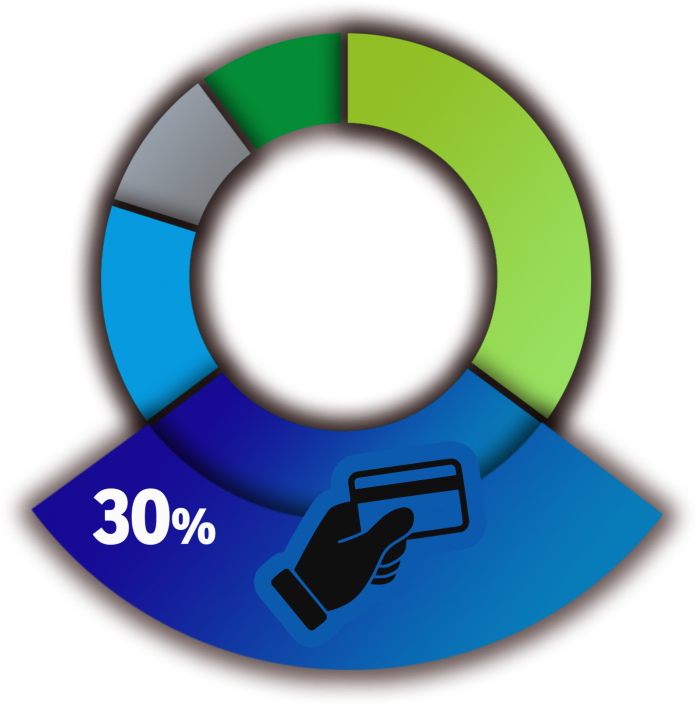

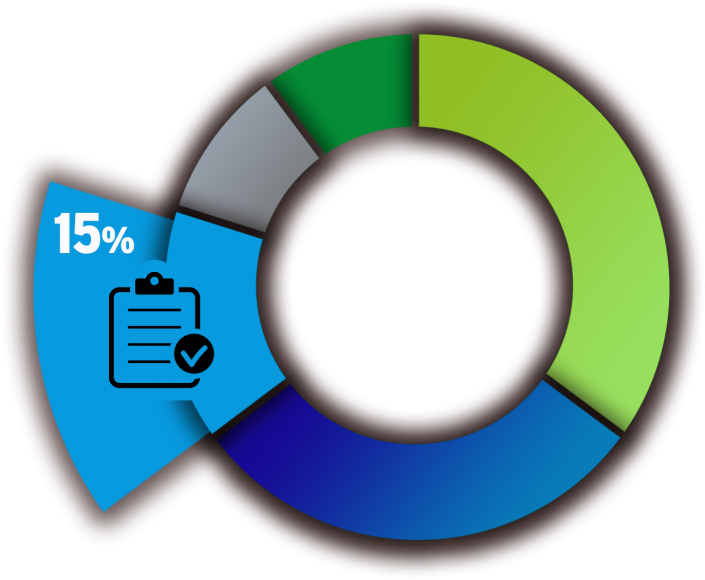

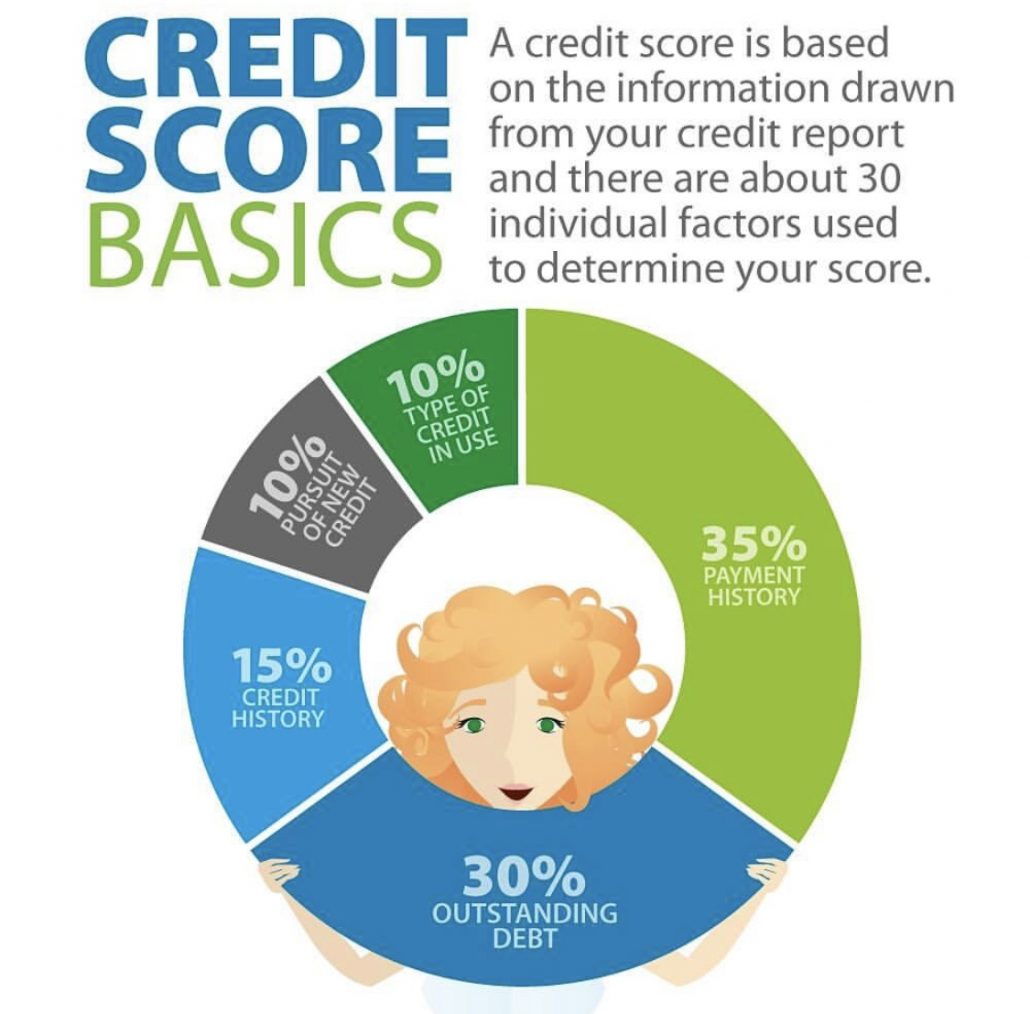

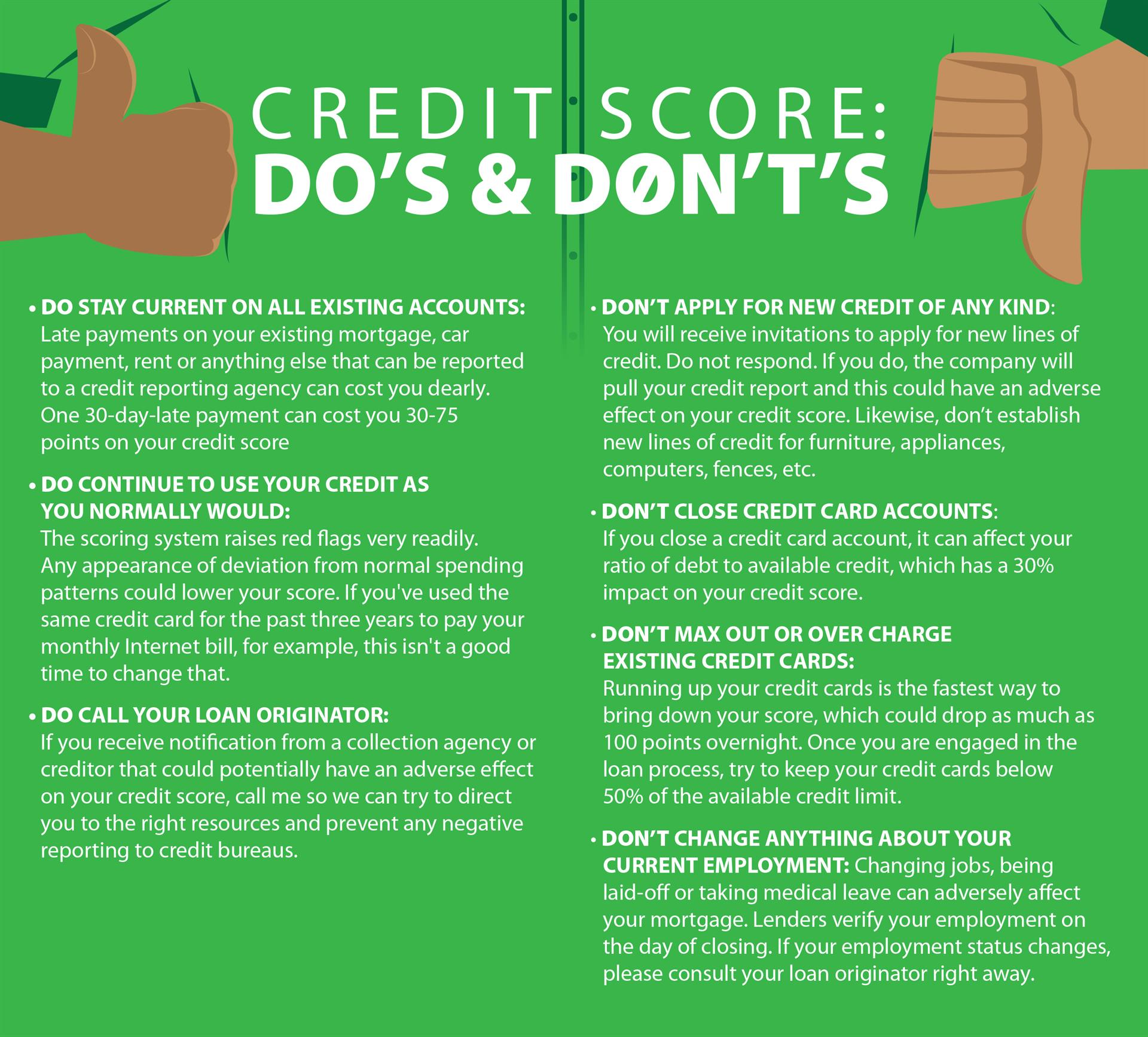

✅ Don’t close your credit accounts. If you must, close the newest ones instead of the oldest ones. Your score will improve over time if you keep accounts open and use them every once in a while.

✅ Think twice before jumping on that latest 0% credit card offer or opening a new card just to get a 10% discount at a department store.

✅ If you don‘t have much of a credit history, and you are planning on taking out a mortgage in the future, it may be a good idea to establish a few open credit lines with little or no balance on them. Although newly opened accounts tend to lower your score initially, they will improve your score once they’ve been open for awhile, somewhat active and paid off with little or no balance.